Review of Results for the Fiscal Year Ended March 2022 (FY2021)

Throughout the fiscal year ended March 31, 2022, (FY2021), the business environment evolved radically. Along with persistent fallout from the COVID-19 pandemic, we have seen a drastic rise in geopolitical risks in the second half as well as hikes in U.S. interest rates and the sharp depreciation of the yen. Amid these circumstances, net income attributable to owners of parent was 109.9 billion yen, falling short of the full-year target of 145.0 billion yen.

In large part, the shortfall in net income reflected (1) the implementation of measures to improve the soundness of our securities portfolio, especially our holdings of foreign bonds, in the fourth quarter. We undertook these measures to ensure our ability to respond in a timely manner to the changes in the business environment based on a reevaluation of risks inherent to such changes in light of their speed and magnitude. Also, we recorded (2) additional credit-related expenses because of a revision of classifications assigned to certain borrowers, further dampening efforts to meet the earnings target.

We take such shortfalls vis-à-vis targets seriously and will intensively explore ways to overcome the issues that are their cause, to this end reexamining our mode of securities management with an eye to restructuring our portfolio. At the same time, we intend to practice financial management focused on curbing risk volume until market conditions stabilize.

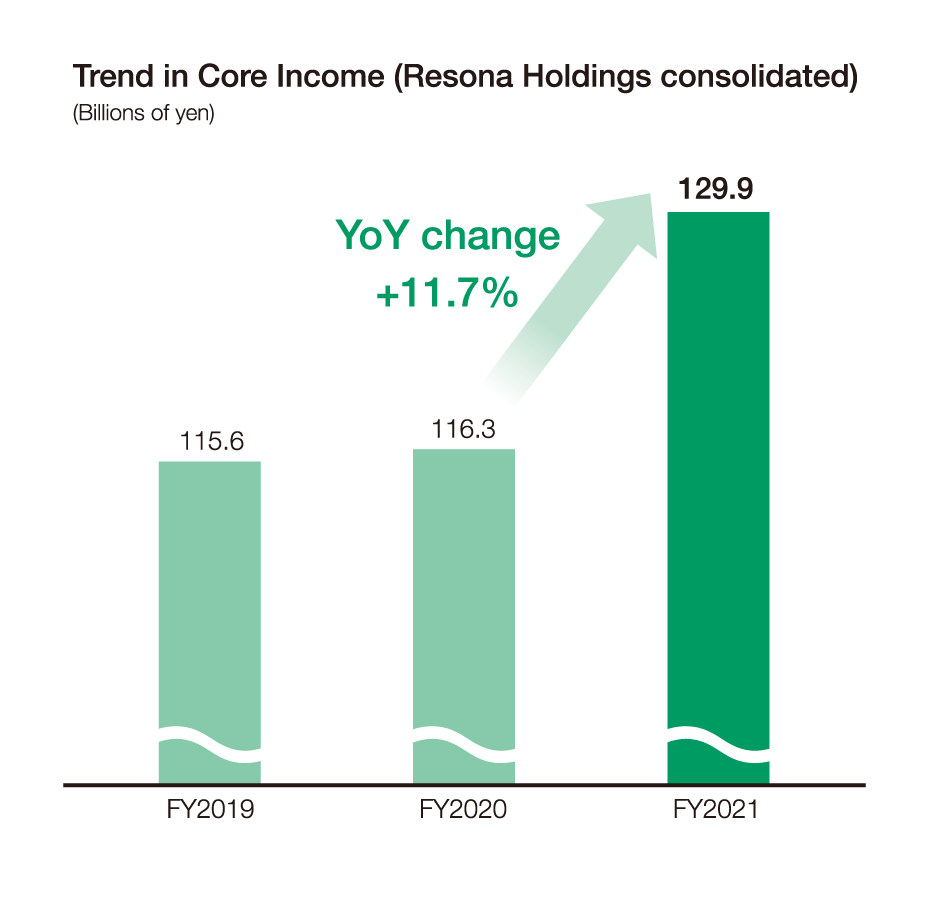

On the other hand, in FY2021, core income (the sum of net interest income from domestic loans and deposits, fee income and operating expenses) increased 13.6 billion yen year on year, continuing an upward trend begun in FY2020 after prolonged stagnation. Moreover, the profit contribution of Kansai Mirai Financial Group (KMFG), which was made a wholly owned subsidiary in April 2021, has grown significantly. Against this background, fee income hit an all-time best since the inauguration of Resona Holdings, while efforts to reduce base expenses progressed steadily. In sum, we have made solid progress in our income and cost structure reforms.

- Secured flexibility supporting the restructuring of our portfolio as well as its soundness in preparation for further interest rate hikes in the future

→Recorded relevant losses totaling 55.0 billion yen in the fourth quarter

- Revised classifications assigned to certain borrowers

→Recorded additional credit-related expenses totaling 38.1 billion yen in the fourth quarter

- No credit extended to businesses in Russia, Ukraine and Belarus

→Stepped up the monitoring of cr edit status via, for example, increased screening in sectors subject to indirect impact

- Special reserve recorded in connection with the COVID-19 pandemic: 8.8 billion yen as of March 31, 2022

Forecast for the Fiscal Year Ending March 2023 (FY2022)

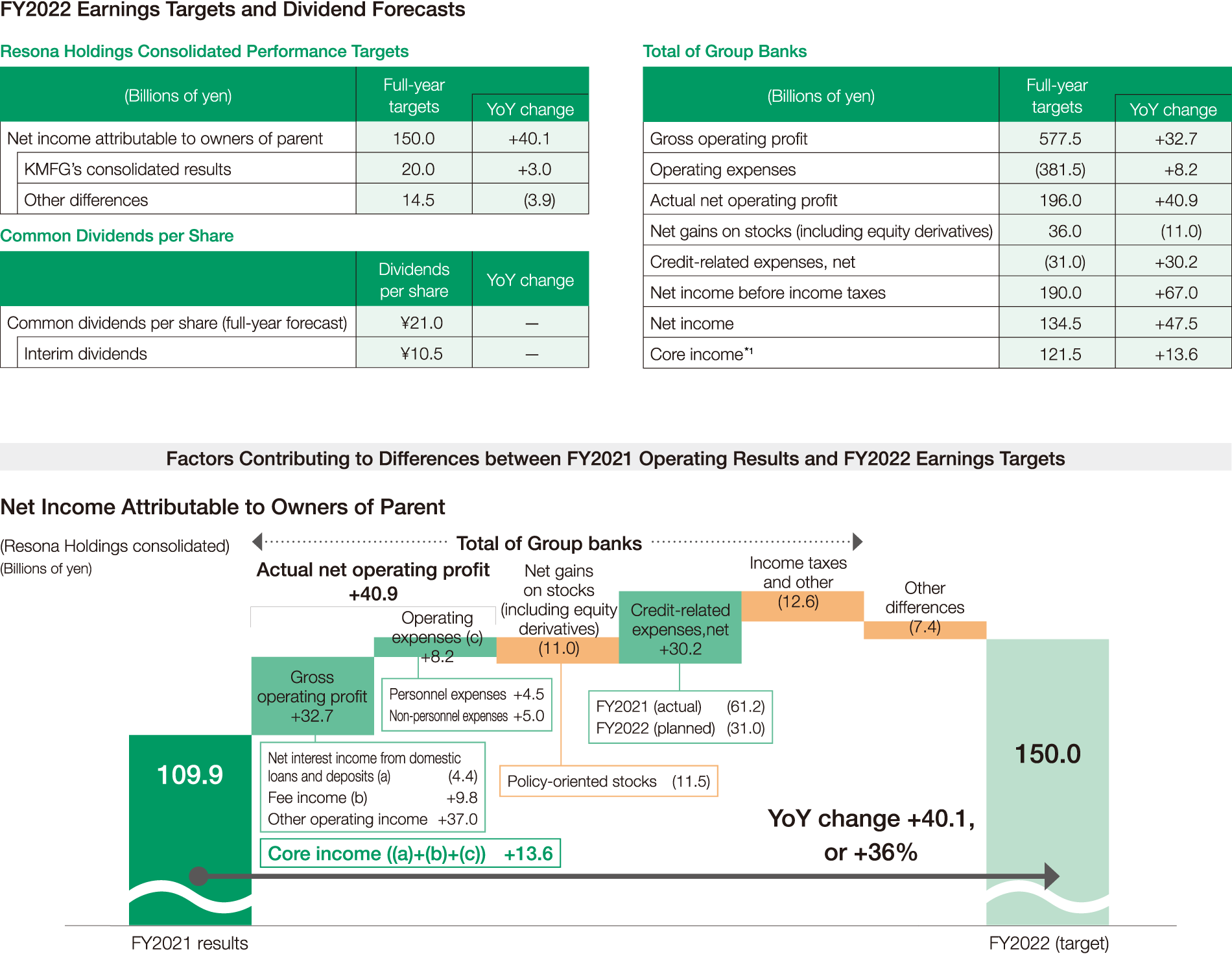

For FY2022, we revised our target for net income attributable to owners of parent to 150.0 billion yen, a 40.1 billion yen year on year improvement from fiscal 2021, while our forecast for common dividends per share amounts to 21 yen per share, unchanged from FY2021.

The previous FY2022 target for net income attributable to owners of parent under the current medium-term management plan (MMP) was 160.0 billion yen and our fresh target represents a downward revision of 10.0 billion yen. When determining this revision, we took into account the detrimental effects on profit of costs associated with additional measures to improve the soundness of our securities portfolio as well as our current policy of focusing on risk mitigation for the time being. As the initial effect of the above measures is expected to be a temporary expansion in costs, we will strive to recover profit over the course of the fiscal year and steadily work toward achieving our financial targets.

Moving on, I will explain the earnings targets for FY2022 on a total of Group banks basis. Gross operating profit is expected to reach 577.5 billion yen, a 32.7 billion yen increase from FY2021. Looking at factors affecting gross operating profit, net interest income from domestic loans and deposits is expected to edge down in step with a slight decrease in the loan rate. However, we expect to see growth in fee income from the asset formation support business, which comprises investment trusts, the fund wrap and insurance, as well as fee income from real estate, M&A and other succession-related operations. Furthermore, other operating income is likely to expand due primarily to the absence of costs associated with measures taken to improve the soundness of our securities portfolio in FY2021.

Operating expenses are expected to be down 8.2 billion yen compared with FY2021 results to 381.5 billion yen. Similarly, personnel and non-personnel expenses are likely to decline 4.5 billion yen and 5.0 billion yen, respectively, from a year earlier. The expected improvement in the latter item is due mainly to a decrease in deposit insurance premiums on the back of the downward revisions of premium rates. Going forward, we will maintain tight control on expenses and, to this end, strive to reduce base expenses even as we step up strategic investments.

Taking the above factors into account, we expect core income to increase 13.6 billion yen from FY2021 while aiming to raise actual net operating profit to 196.0 billion yen, up 40.9 billion yen year on year.

On the other hand, we forecast that net gains on stocks (including equity derivatives) will decline 11.0 billion yen year on year to 36.0 billion yen.

Although we intend to accelerate the reduction of policy-oriented stockholdings on an acquisition price basis, the above forecast factors in a recoil arising from the absence of FY2021 proceeds from sales of stocks with high unrealized gains.

We forecast that credit-related expenses will amount to 31.0 billion yen, a decrease of 30.2 billion yen from FY2021, due mainly to the absence of an additional reserve recorded in said fiscal year in connection with major clients. In addition, none of the Group banks have direct exposure to credit risks related to either Russia or Ukraine. However, businesses run by our customers may be indirectly affected in diverse ways, for example, via lingering supply restrictions. With this in mind, we will maintain in-depth dialogue with our customers while strengthening our monitoring for signs of credit risk, so that we can better support their business management.

We aim to raise the consolidated fee income ratio, a key performance indicator (KPI) under the MMP, to around 35% in FY2022 from 34.6% recorded in FY2021, with an eye to achieving a consolidated fee income ratio of 35% or more in the final year of the MMP.

With regard to the consolidated cost income ratio, we aim to eventually curb the ratio at around 60% under the MMP and, to this end, are working to improve it to lower half of the 60% range in FY2022 from the 69.1% recorded in FY2021.

To successfully close FY2022, the final year of the MMP, we will strive to deliver solutions aligned with changes in issues customers are confronting in the fields of sustainability transformation (SX) and digital transformation (DX) while rebuilding our foundations for the entire Group and accelerating the creation of synergies with KMFG. In these and other ways, we will promote income and cost structure reforms and ensure that they yield tangible progress to be reported to our stakeholders.

- *1Net interest income from domestic loans and deposits + Fee income + Operating expenses

Reduction in Policy-Oriented Stockholdings

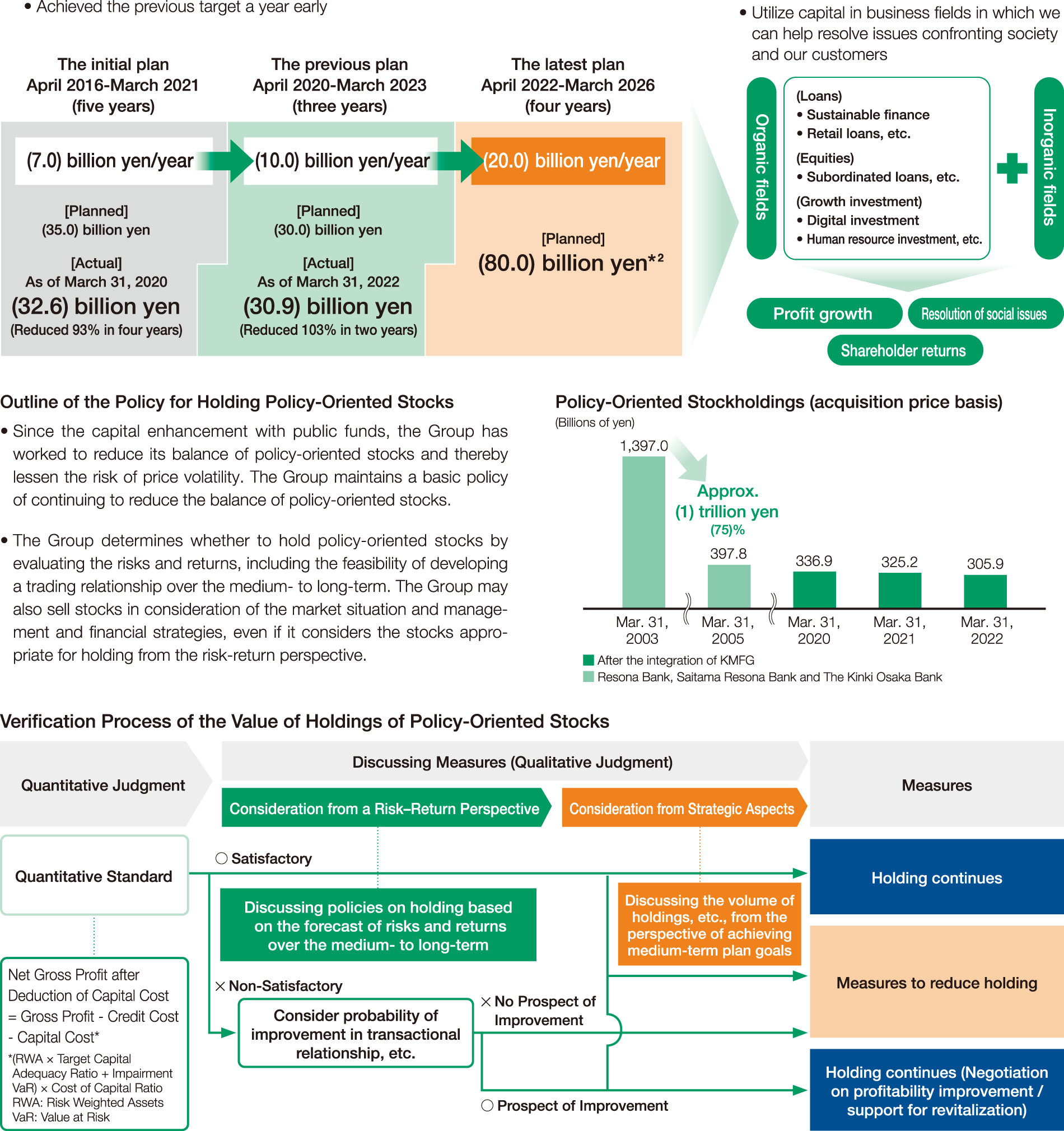

Since the 2003 injection of public funds, we have reduced our holdings of policy-oriented stocks by approximately 1 trillion yen via a course of financial reform, well ahead of other Japanese banks. As such, we have focused on reducing our exposure to equity price fluctuation risk.

In recent years, we have steadily reduced our policy-oriented stockholdings in line with a target of reducing such stockholdings by approximately 35.0 billion yen over a five-year period (7.0 billion yen/year) that began in April 2016. Having achieved a reduction totaling 32.6 billion yen, or 93% of this target, in the first four years, in May 2020 we revised the target, announcing a new goal of reducing such stockholdings by a further 30.0 billion yen in the three-year period (10.0 billion yen/year) beginning April 2020, accelerating the pace of reduction.

Once again, we were ahead of schedule, successfully achieving a 103% or 30.9 billion yen reduction and surpassing the three-year target in two years. So, in May 2022, we set another new target and now aim to reduce policy-oriented stockholdings by 80.0 billion yen over the course of the four years leading up to March 31, 2026. This represents an annual reduction of 20.0 billion yen, with the pace of reduction set for twice that of the previous target.

It should be noted that comparisons between the acquisition price and the market value of our current portfolio of policy-oriented stocks reveal that the market value of the latest group of stockholdings targeted for reductions over the course of the next four years is approximately 250.0 billion yen. In this way, we will continuously strive to reduce our policy-oriented stockholdings under the new target, pursuing reductions at an even faster pace.

Looking ahead, we will utilize capital freed up via the reduction of policy-oriented stocks to pursue robust organic and inorganic growth, especially in business fields in which we can help resolve issues confronting society and our customers.

◎A new target aiming for reductions at a doubled pace announced (May 2022)

◎With regard to the exercise of voting rights associated with policy-oriented stocks, we established the Standards for the Exercise of Voting Rights of Policy-Oriented Stocks, securing a structure for supporting proper voting judgment on individual agenda items and verifying such judgment

- The Resona Group’s fundamental stance on the exercise of voting rights (excerpt from the above standards)

- (1)Irrespective of interests of transactions with clients, make an effort to vote yes or no on an individual basis from the viewpoint of sustainably improving corporate value;

- (2)Not to exercise voting rights in a manner to resolve certain political or social problems; and

- (3)If any scandal or an anti-social act is committed by a company or corporate manager, etc., exercise voting rights with the intention of contributing to the improvement of corporate governance.

- *2Reference: Approximately 250.0 billion yen on a market-value basis (calculated based on the market value of the Group’s policy-oriented stockholdings as of March 2022)

Tax-Compliance Initiatives

The Resona Group upholds a basic policy of complying with the tax-related laws and regulations enforced in all countries and regions in which it undertakes business activities and is committed to appropriately fulfilling its taxpayer responsibilities with respect for the spirit as well as the rule of such laws and regulations. Accordingly, the Group has established and announced a Tax Policy as outlined below.

Basic Policy

In line with the Resona Standards, the Resona Group shall comply with tax-related laws and regulations while appropriately managing tax-related expenses via the maintenance of a proper tax compliance structure, with the aim of improving its corporate value.

Also, the Resona Group shall take proper action aimed at ensuring that its business bases maintain appropriate tax compliance in conformity with the laws and regulations enforced by countries and regions in which they operate and that they abide by international taxation guidelines announced by relevant authorities.

Capital Management

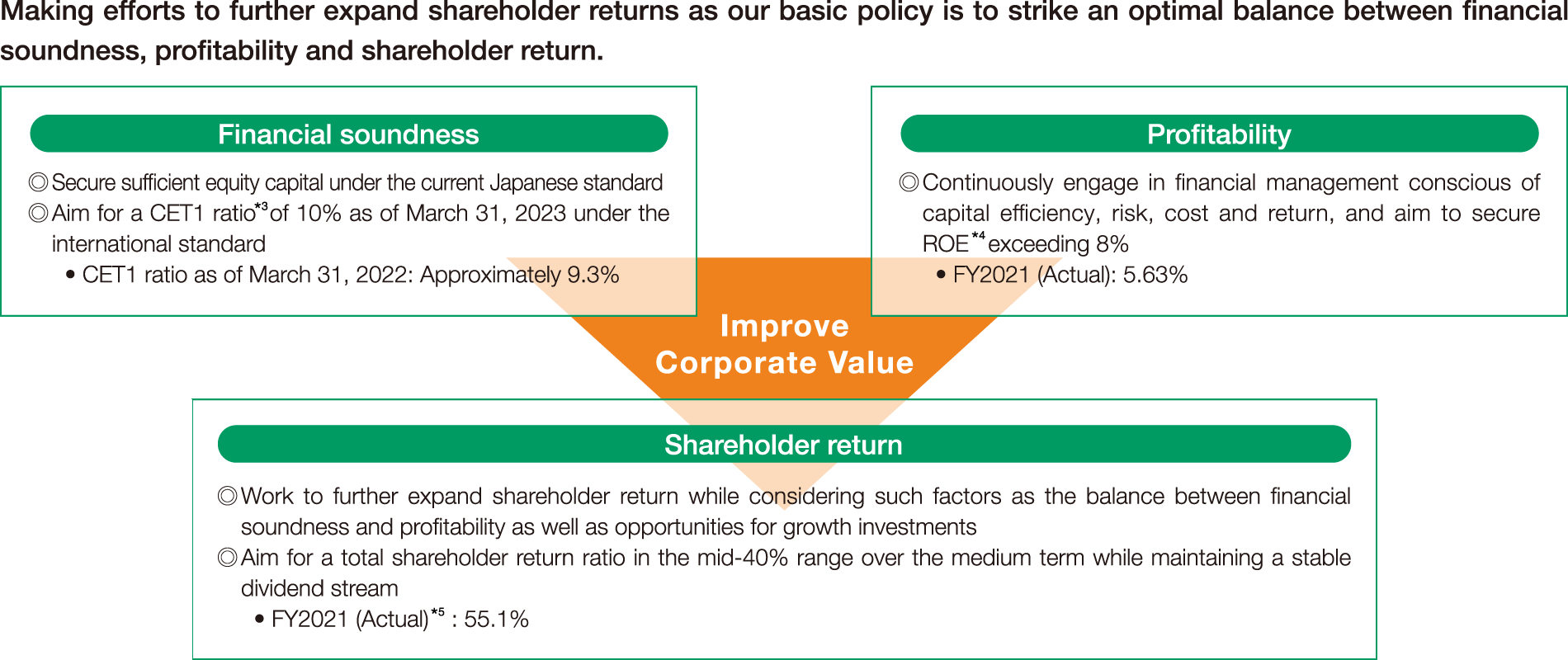

In line with its basic capital management policy, the Resona Group aims to maintain an optimal balance between 1) financial soundness, 2) profitability and 3) shareholder return. In addition to maintaining a stable stream of cash dividends, we aim for a total shareholder return ratio in the mid-40% range over the medium term. In these ways, we will strive to further enhance shareholder returns in a way that balances financial soundness and profitability as well as giving due consideration to seizing growth investment opportunities.

As of March 31, 2022, our Common Equity Tier 1 (CET1) capital ratio (based on regulations to be effective upon the enforcement of the finalized Basel 3; excluding net unrealized gains on available-for-sale securities), which indicates financial soundness, stood at around 9.3%. We expect this ratio to increase to the higher half of the 9% range by the end of FY2022. In addition, ROE (based on total shareholders’ equity), a profitability indicator, was 5.63% in FY2021. For FY2022, we anticipate that ROE will grow to the mid-7% range. ROE did not reach 8%, our target under the MMP, in FY2021 and nor is it likely to reach this target in FY2022 due to the inclusion of actual and estimated costs arising from measures to secure timely response to inherent risks. However, we will push ahead further with income and cost structure reforms and enhance our earnings power while steadily raising capital productivity through the effective utilization of capital.

As for shareholder returns, we executed a share buyback in November 2021, expending approximately 10.0 billion yen, based on our determination to establish a clear roadmap toward the achievement of our shareholder return target.

Since the injection of public funds in 2003, the Resona Group has striven to improve the quality of its capital and, even after the full repayment of public funds in 2015, worked to accumulate a robust volume of capital. Now, we believe that we are about to enter a new phase in which we can step up the utilization of capital. Going forward, we aim to accelerate capital circulation aimed at enhancing our corporate value and, to this end, intend to engage in robust in-house discussions with an eye to incorporating relevant measures into the next MMP.

- *3Based on regulations to be effective upon the enforcement of the finalized Basel 3; excluding net unrealized gains on available-for-sale securities

- *4Net income attributable to owners of parent / Total shareholders’ equity (simple average of the balances at the beginning and end of the term)

- *5Excluding a share buyback undertaken to neutralize the dilutive effect on EPS of making KMFG a wholly owned subsidiary

Dialogue with Shareholders and Investors

We also place emphasis on maintaining constructive dialogue with shareholders and investors. Seeking to secure sustainable corporate growth and medium- to long-term improvement in the Group’s corporate value, we strive to ensure that our shareholders and investors have an accurate understanding of, confidence in and a fair evaluation of the Group’s management strategy and financial condition and engage them in various forms of discussion to garner their input, which we reflect in our actions.

Due to the COVID-19 pandemic, as in the previous year, opportunities for face-to-face dialogue were somewhat limited in FY2021. Nevertheless, we have striven to expand opportunities for dialogue via digital platforms, remote interviews with shareholders and investors, online shareholder seminars and web-based briefings for individual investors. We also launched YouTube-based video streaming programs for individual investors.

Opinions voiced by shareholders and investors are regularly reported to the Board of Directors and other bodies to improve our management strategy. At the same time, we endeavor to facilitate employee understanding of the market reputation of and market expectations regarding the Resona Group’s business performance.

In addition, one of our aims under the MMP is to ensure our ongoing inclusion in all four of the ESG indices selected by the Government Pension Investment Fund (GPIF). To that end, we are constantly enhancing the content of information disclosure, including disclosure related to our SX initiatives and other non-financial information. In addition, in our efforts to disclose information fairly and impartially, we remain conscious of the need to reduce capital costs through the elimination of informational asymmetry. In these ways, we strive to enhance the content of dialogue with shareholders and investors.