Review of Results for the Fiscal Year Ended March 2025 (FY2024) and the Outline of FY2025 Annual Plan

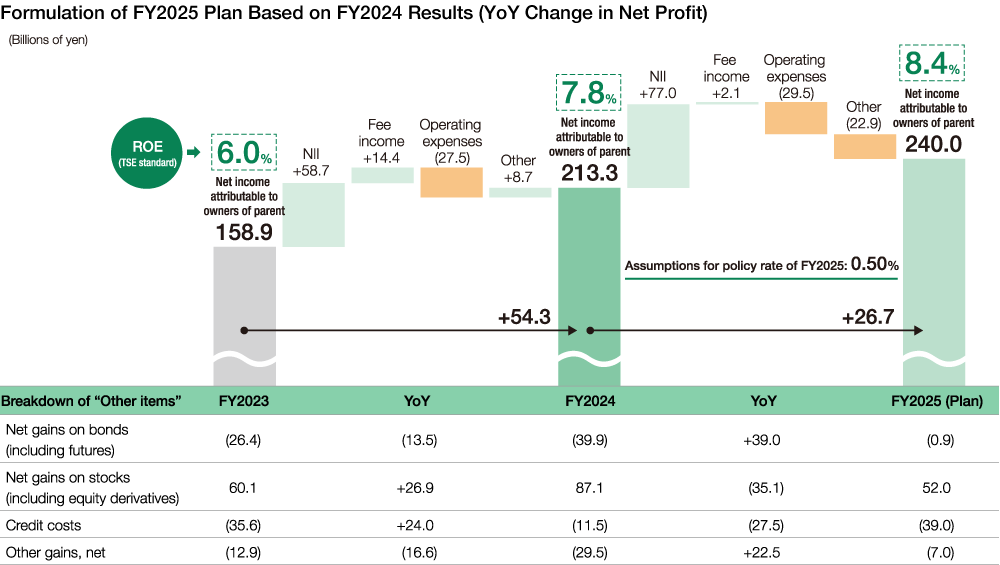

In the fiscal year ended March 31, 2025, the Japanese economy remained on a modest recovery track, while the Bank of Japan (BOJ) made a shift in its monetary policy. Against this backdrop, net income attributable to owners of parent amounted to 213.3 billion yen, an increase of 54.3 billion yen from the previous fiscal year. Thus, we achieved net income exceeding 200.0 billion yen for the first time in seven fiscal years since FY2017.

We are presently aiming for net income attributable to owners of parent of 240.0 billion yen, a year-on-year increase of 26.7 billion yen, for FY2025. This target is based on an assumption that the policy rate will be kept at 0.5%. In addition, our consolidated gross operating profit target is set at 800.0 billion yen. We will achieve this target and hit a record high for this indicator for the first time in 19 fiscal years since FY2006 by taking full advantage of the accumulation of positive effects arising from interest rate hikes while expanding the loan balance and other assets.

In FY2024, our ROE based on total stockholders’ equity, which is set as a KPI for the medium-term management plan (MMP), amounted to 9.3%. Having thus satisfied our 8% target for the final year of the MMP a year ahead of schedule, we are now aiming for an ROE of 10% for FY2025. Furthermore, in FY2025 we began disclosing an ROE target value based on the TSE standard. When calculated using this standard, our ROE in FY2024 amounted to 7.8%, while our ROE target is set at 8.4% for FY2025.

Moving on, I will discuss factors contributing to differences between FY2024 results and FY2025 plans. In FY2024, we were able to raise core net operating profit by expanding top-line income and offsetting growth in operating expenses via the use of the two income sources, namely, net interest income (NII) and fee income. With the inflationary environment taking hold, expense management is of greater importance than ever before. To secure a solid path toward sustainable growth in the future, we will push ahead with the DX-driven overhaul of our business processes even as we continue to undertake proactive investment in human resources and IT infrastructure. Through these initiatives, we aim to stably achieve positive outcomes in terms of enhancing operational productivity and efficiency.

Looking at factors associated with non-recurring gains and losses, the divestment of our policy-oriented stockholdings progressed, while credit costs remained low. Also, we collectively recognized expenses arising from the integration of Minato Bank’s back-office operations and systems in the fourth quarter, taking advantage of favorable financial results backed by excess profit as well as robust income from our main business. Moreover, we executed a strategic reshuffling of our securities portfolio. Through these and other measures, we have striven to increase our future profitability. After absorbing the outflows arising from the activities named above, net income attributable to owners of parent still exceeded our target (as announced in November 2024) by more than 20%.

Looking at our FY2025 annual plan, we expect full-year operating results to benefit from the ongoing robustness of top-line income supported by the two income sources and include year-on-year profit growth due to the absence of losses on bonds and extraordinary losses recorded in FY2024. On the other hand, this plan factors in the impact of U.S. tariffs, an increase in geopolitical risks and other variables that could make the business environment murkier. Accordingly, our assumptions include the reduction of net gains on stocks and growth in credit costs, and, therefore, are generally prudent in terms of the extent of extraordinary gains we could earn.

On the facing page, the factors contributing to differences between FY2024 results and FY2025 plans are presented in the form of a bar graph and table. Please note that the Breakdown of “Other items” includes the details of a substantial year-on-year change.

Initiatives to Improve Corporate Value

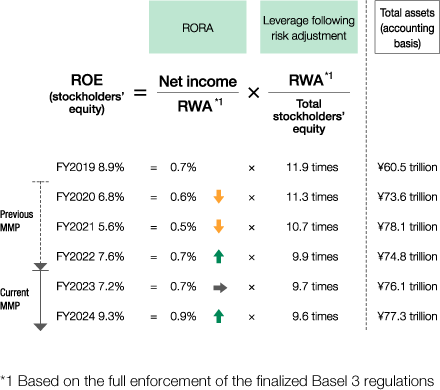

Next, I will discuss our initiatives to improve corporate value. To improve the price book-value ratio (PBR), an indicator for measuring market ratings, it is important to pursue both 1) higher ROE and 2) lower capital costs. Here, I deliver supplementary information regarding our ROE target in addition to sharing our analysis results on its two primary components: return on risk-weighted assets (RORA) and leverage following risk adjustment. The actual ROE result is presented based on total stockholders’ equity.

Over the course of the first two years of the previous MMP period, despite recovering in the final year of the MMP, ROE was on a downturn trend. Due to a substantial increase in the deposit balance during the COVID-19 pandemic, the Group’s balance sheet had expanded rapidly, with the volume of low-profitability assets becoming larger. Amidst these circumstances, we recognized a considerable volume of credit costs while executing measures to improve the soundness of the foreign bond portfolio. These and other factors, in turn, resulted in an ongoing decline in RORA, keeping ROE low.

Under the current MMP, we have taken a more proactive balance sheet management approach with the aim of improving risk return. In FY2024, the volume of loans grew substantially, while the Group benefitted from a significant increase in net interest income, which was robustly supported by a tailwind arising from interest rate hikes. In addition, fee income hit an all-time best for the fourth consecutive fiscal year. These are primary factors contributing to a higher RORA, which, in turn, enabled us to raise ROE. We will strive to achieve even better results in FY2025.

While the world with interest rates is taking hold, financial institutions like us are now confronting the major issue of securing stable deposits. In this regard, however, the Resona Group’s competitive edge will remain viable as it has the advantage of a robust branch network rooted in the Tokyo metropolitan and other urban areas as well as a solid customer base encompassing a great number of retail customers. Accordingly, we will continue striving to increase highly sticky deposits by delivering overwhelming service convenience backed by digital technologies while taking full advantage of our existing network of physical branches and other face-to-face customer contact points.

Impact of the Yen Interest Rate Hikes on Profit (provisional calculation)

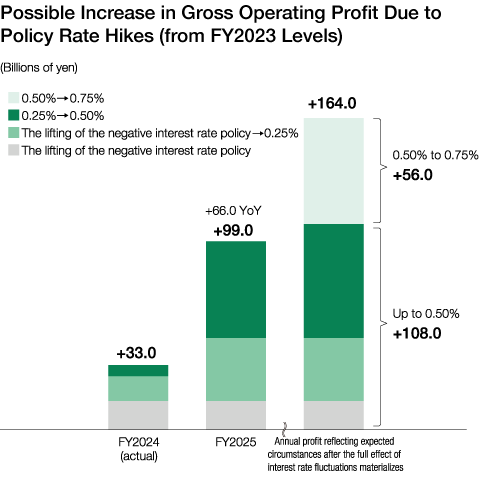

The Resona Group’s balance sheet is often considered by investors to be relatively sensitive to interest rates. Because of this, I have received questions from a number of people regarding how much the Group’s profit will be affected if the BOJ’s monetary policy shifts even further. The provisional calculation of the impact of such a shift could differ greatly depending on various assumptions, which include a number of variables from the timing and pace of a monetary policy shift to the degree of such a shift. As a reference, we disclose the estimated impact of the policy rate hike on gross operating profit (compared with the FY2023 level) as below. This reference is formulated using a simplified calculation method that does not take changes in the balance of assets and liabilities into account.

If the BOJ had raised the policy rate to a maximum of 0.5%, top-line income for FY2024 would have benefitted from a positive effect of 33.0 billion yen. The cumulative total profit effect to be available over the course of the two fiscal years leading up to the end of FY2025, is estimated at around 99.0 billion yen. The impact on the single-year top-line income for FY2025 alone could, therefore, amount to 66.0 billion yen, twice as much as the hypothetical impact on FY2024 top-line income. Furthermore, if we fully enjoy benefits arising from the policy rate hike to a maximum of 0.5%, the two-year cumulative positive effect will amount to 108.0 billion yen.

In addition, if the policy rate were to be raised further to 0.75%, the positive effects would include an additional increase of 56.0 billion yen in top-line income, with the overall cumulative profit effect totaling 164.0 billion yen. If this scenario comes into play, we could expect to record an ROE of 10% based on the TSE standard, considering the current level of capital. As fluctuations in the balance of assets and liabilities are not considered in the above estimates, we may well enjoy even greater upsides. That being said, these estimates are merely a result of the analysis of the policy-rate sensitivity of our top-line income based on certain assumptions. Readers are advised to consider the fact that our calculations exclude possible growth in operating expenses, credit costs, etc. on the back of persistent inflation.

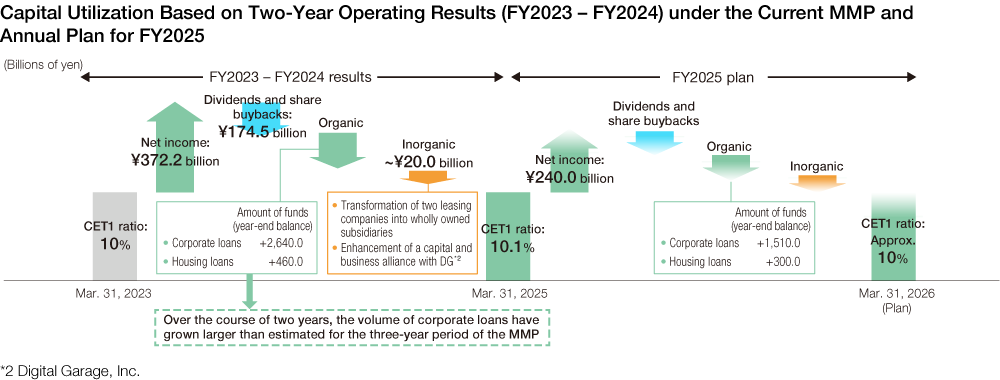

Capital Allocation

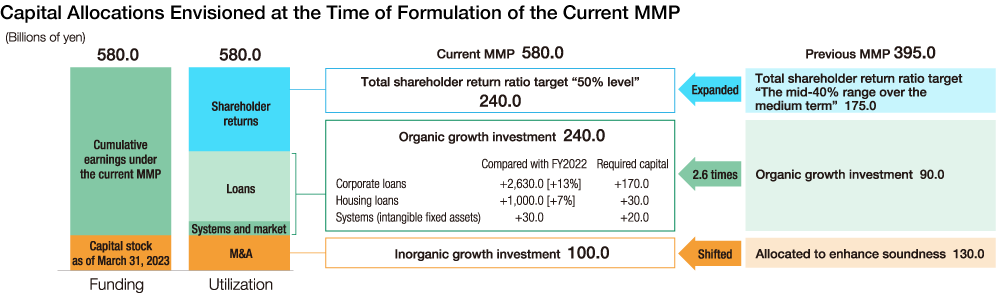

Under the current MMP, we have entered into a phase of full capital utilization, transitioning away from our traditional focus, which, until the close of the previous MMP, had been placed on achieving the qualitative and quantitative enhancement of capital. Our goal now is to pursue improvement in corporate value by utilizing capital to undertake growth investment and to enhance the content of shareholder returns in a way that maintains financial soundness. The two graphs presented at the top of the facing page show an overview of capital allocations envisioned at the time of the formulation of the current MMP as well as how we will utilize capital based on operating results achieved thus far over the course of the first two years of this MMP and our plan for FY2025. As profit has remained higher than planned, the volume of growth investment has expanded faster than estimated at the time of the formulation of the MMP, especially with regard to organic growth investment, an area in which we are leaning toward the enhancement of high-quality loans mainly targeting corporate borrowers.

Taking these factors into account, our Common Equity Tier 1 (CET1) capital ratio* amounted to 10.18% as of March 31, 2025, stably within the 10% range. Looking ahead, we will enhance the content of shareholder returns while maintaining a robust level of financial soundness. Simultaneously, we will promote capital utilization in both organic and inorganic growth fields so that we can report sustainable growth in operating results to our stakeholders.

- * Based on the full enforcement of the finalized Basel 3 regulations under the international standard; excluding net unrealized gains on available-for-sale securities

Shareholder Return Policy

In May 2025, we partially revised our shareholder return policy in light of changes in internal and external environments. Here, I explain our thoughts behind this move.

Until the end of FY2024, we had positioned enhancing the content of shareholder returns as an issue that must be tackled to optimize the number of shares outstanding as part of capital management. Therefore, we had traditionally focused on undertaking share buybacks to enhance the content of shareholder returns even as we gave due consideration to balancing funds allocated to these measures with the volume of dividends.

When revising our shareholder return policy, we took into account the three points described below in light of changes in internal and external environments: 1) we may anticipate stable growth in our earnings power on the back of the return of the world with interest rates; 2) we could face greater volatility in extraordinary gains and losses over the course of the period covered by our plan for the divestment of policy-oriented stockholdings (until March 31, 2030); and 3) we need to increase the dividend-based appeal of our shares. As a result, our revised policy is to stably increase the volume of dividends, with a DOE of approximately 3% newly defined as a dividend-related indicator for FY2029, even as we continuously aim for our total shareholder return target of around 50%.

The Company also intends to stay focused on divesting its policy-oriented stockholdings until March 31, 2030. Given this, the deadline for the achievement of our DOE target is set at FY2029 so that the volume of dividends may be increased at a steady pace regardless of the volume of gains on policy-oriented stocks to be divested during the above period. Thus, over the course of five years going forward, we will endeavor to increase our DOE to approximately 3%, roughly 1.5 times the current level. If needed, we may also consider revising our DOE target by giving due consideration to the level of profit, the status of stock prices, feedback from the market and other input. In line with our renewed policy, we will also continue to undertake share buybacks. Thus, through the expansion of profit and the optimization of the number of shares outstanding, we will stably increase earnings per share (EPS).

- FY2024

-

- (1) Increased year-end dividends per share:

Up 2 yen from the forecast (11.5 yen -> 13.5 yen)

Resulting in an YoY increase of 3 yen per share in full-year dividends (FY2023: 22 yen -> FY2024: 25 yen)

- (1) Increased year-end dividends per share:

- FY2025

-

- (2) Dividend forecast per share: Full-year dividends of

29 yen, up 4 yen YoY (FY2024: 25 yen -> FY2025: 29 yen) - (3) A maximum of 30.0 yen billion budget set aside for share buybacks

Funds set aside for share buybacks: Up to 30.0 billion yen

Share buyback period: May 14 to July 31, 2025

- (2) Dividend forecast per share: Full-year dividends of

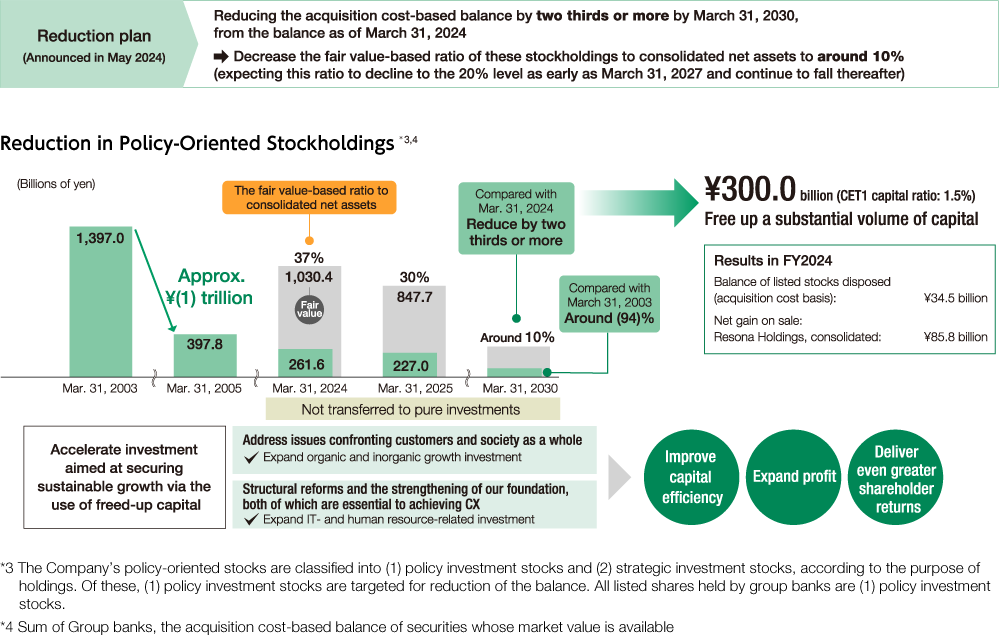

Reduction in Policy-Oriented Stockholdings

Since the 2003 injection of public funds, we have shrunk our holdings of policy-oriented stocks via a course of financial reform, well ahead of other Japanese banks, achieving a reduction amounting to approximately 1 trillion yen (acquisition cost-basis, as of March 31, 2005). Even after this accomplishment, we have been engaging in robust negotiations with corporate customers to reduce our holdings of such stocks. In FY2024, we launched a new six-year plan to this end.

The new plan is focused on securing the management resources necessary for the creation of new customer value even as we achieve sustainable growth for ourselves. We will utilize capital freed up via the reduction of policy-oriented stocks to secure our ability to address issues customers and society as a whole are confronting as well as to accelerate structural reforms and the strengthening of our foundations, both of which are essential to achieving CX (corporate transformation). The new plan will also facilitate the virtuous cycle of capital circulation that will, in turn, yield upsides on profit. Drawing on this positive effect, we will sustainably expand the volume of shareholder returns.

Under the new plan, we aim to reduce our policy-oriented stockholdings on an acquisition cost basis by two thirds or more by the end of March 2030. We also aim to reduce them by approximately the same amount on a fair value-basis. Accordingly, we will decrease the fair value-based ratio of these stockholdings to consolidated net assets to around 10%. We expect this ratio to decline to the 20% level as early as March 31, 2027, and continue to fall thereafter. Over the course of FY2024, the first year of the plan, we reduced policy-oriented stockholdings totaling 34.5 billion yen on an acquisition cost-basis.

Also, we autonomously exercise voting rights associated with policy-oriented stocks in accordance with the “Basic Concepts on the Exercise of Voting Rights” and “Guidelines for the Exercise of Voting Rights” while providing the Board of Directors with reports on the status of the exercise of such rights on an annual basis.

Dialogue with Shareholders and Investors

We deem it extremely important to maintain constructive dialogue with shareholders and investors. Seeking to secure sustainable corporate growth and medium- to long-term improvement in the Group’s corporate value, we strive to ensure that our shareholders and investors have an accurate understanding of, confidence in and are able to fairly evaluate the Group’s management strategy and financial condition. This is why we engage them in various forms of discussion to garner their input, which we reflect in our actions.

In FY2024, we proactively created a growing number of opportunities for such dialogue. For institutional investors, we held financial results briefings, individual meetings, small-scale meetings and other events to ensure ongoing dialogue. We similarly took a proactive approach to overseas investor relations (IR) dialogues. Through these activities, the number of investors we interviewed grew a substantial 1.4 times from the previous fiscal year. For individual investors, we held online briefings and shareholder seminars while reaching out to them via streaming on YouTube. In these and other ways, we leveraged face-to-face and digital channels to enhance opportunities for investors to stay up-to date with our operational status.

Opinions voiced by shareholders and investors are regularly reported to the Board of Directors and other bodies to improve our management strategy. At the same time, we endeavor to facilitate internal understanding of the market reputation of and market expectations regarding the Resona Group’s business performance. Currently, vigorous discussion is under way to formulate a new MMP to be launched in FY2026. Looking ahead, we will continue heeding opinions, insights and other input from shareholders and investors as we address these and other topics.