Related Policies

Policy for Holding Policy-Oriented Stocks

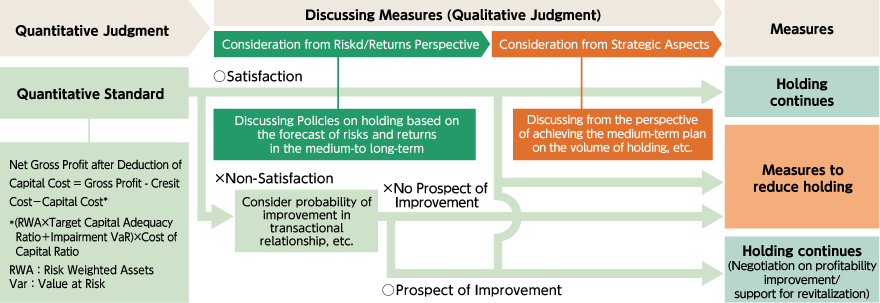

- Since the capital enhancement with public funds, the Resona Group has been negotiating with customers, trying to reduce the balance of the policy-oriented stocks, and has made efforts to lessen the risk of price volatility. Our basic policy is to continue to reduce the balance of the policy-oriented stocks, taking into account changes to the business environment such as the Corporate Governance Code.

- In holding policy-oriented stocks, the Resona Group aims to continuously enhance corporate value of the customers and the Group. The Group determines whether to hold policy-oriented stocks by evaluating the risks and returns, including feasibility of the development of a trading relationship in a medium-to long-term.

- When the Resona Group determines that it is not appropriate to hold certain policy-oriented stocks after such verification process, it will proceed to sell these stocks with sufficient understanding of the customers through communications. We will pursue negotiations for the sale through constructive dialogue with our clients, aiming to enhance sustainable corporate value and address underlying issues, even though the Group considers appropriate for holding from the risk-return perspective.

Standards for the Exercise of Voting Rights of Policy-Oriented Stocks

1. Fundamental Concepts on the Exercise of Voting Rights

The Resona Group will exercise voting rights of policy-oriented stocks based on the following policy:

- (1)Irrespective of interests of transactions with clients, make an effort to vote yes or no on an individual basis from the viewpoint of sustainably improving corporate value;

- (2)Not to exercise voting rights in a manner to resolve certain political or social problems; and

- (3)If any scandal or an anti-social act is committed by a company or corporate manager, etc., exercise voting rights with the intention of contributing to the improvement of corporate governance.

2. Guidelines for the Exercise of Voting Rights

With the aim of exercising its voting rights in an appropriate and efficient manner, the Resona Group will abide by the following guidelines.

- (1)Base voting judgments on the following points

-

- a.Whether the way the vote is cast helps the Company and/or the investee achieve sustainable and long-term growth in corporate value

- b.Whether the way the vote is cast is consistent with the overall interest of shareholders

- (2)In particular, before casting a yes or no vote on one of the following types of agenda items, give due consideration to whether voting contributes to growth in the investee’s corporate value

-

- a.Shareholder proposals

- b.Introduction or renewal of anti-takeover measures

- c.Agenda items proposed by a corporation that was found to be implicated in a scandal or an anti-social act

- d.Approval of financial statements not backed by an unqualified opinion issued by the accounting auditor

- e.Dismissal of directors, accounting auditors, etc.

- (3)When a vote is cast in opposition to the Company’s intention, the Board of Directors will review the status of the exercise of voting rights to confirm whether these guidelines were fully observed. The Company will also strive to increase the sophistication of its exercise of voting rights by, for example, revising these guidelines.

Status of Reduction in Policy-oriented Stocks

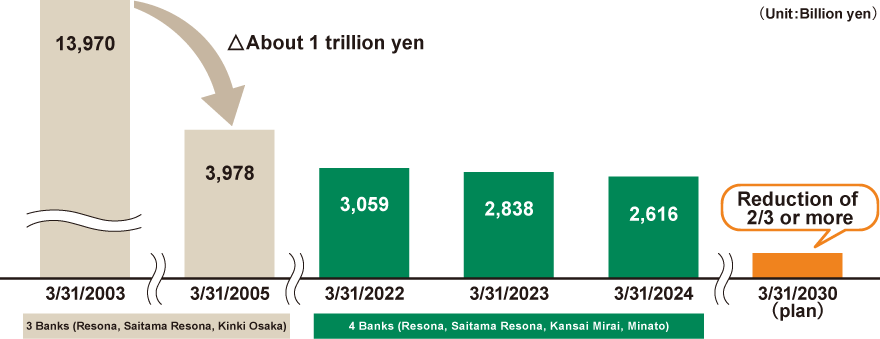

As part of the financial reforms since the injection of public funds in 2003, the Company has reduced the policy-oriented stocks by approximately 1 trillion yen ahead of other companies, and has proceeded with further reductions through negotiations with customers, thereby making efforts to lessen the risk of price volatility.

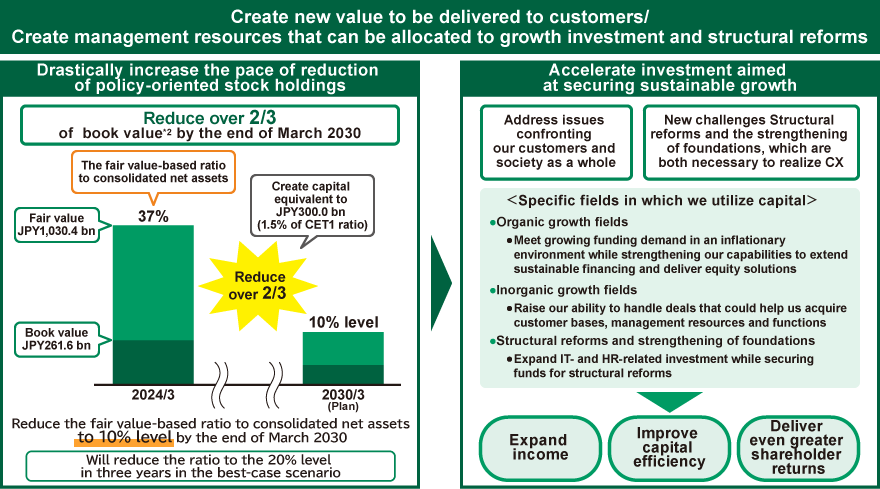

In May 2024, the Company announced a plan to reduce two-thirds or more of the policy-oriented stock on a book value basis by March 2030, and aims their market value to be approximately 10% of the consolidated net assets.

The plan has been implemented steadily. In the fiscal year ended March 2026, the second year of the plan, the reduction amounted to 32.6 billion yen, bringing cumulative progress to 38.5% of the six-year target.

By using funds to be generated through the reduction of the policy-oriented stocks, the Company will accelerate investments for the Group's continuous growth.

Outline of "Basic Policy for Promoting Constructive Dialogues with Shareholders, Investors, etc."

Please visit the following webpage.