Risk Management

Risk Management System

Basic Approach to Risk Management

We deeply regret the serious concern and inconvenience that the application for an injection of public funds in May 2003 caused the people of Japan, our customers, and other stakeholders. Consequently, we have established the three risk management principles shown below to enhance our risk management systems and methods as well as risk control. The Resona Group conducts its risk management activities with an eye to securing the soundness of operations and enhancing profitability.

Three Risk Management Principles

- 1.We will not assume levels of risk in excess of our economic capital.

- 2.We will deal promptly with losses that we have incurred or expect to incur.

- 3.We will take risks appropriate for our earnings power.

Risk Management Policies and Systems

The Resona Group is exposed to various types of risk, including those associated with business strategies, the violation of laws and regulations and systems failures as well as those related to business outsourcing (e.g., suspensions of operations and information leaks involving vendors).

As it aims to appropriately handle these risks in adherence to the three risk management principles, Resona Holdings has established the Group Risk Management Policy. This policy is intended to clarify types and definitions of risks to be managed and the organizational structure for risk management as well as the fundamental risk management framework, with the aim of developing a robust risk management system for the Group.

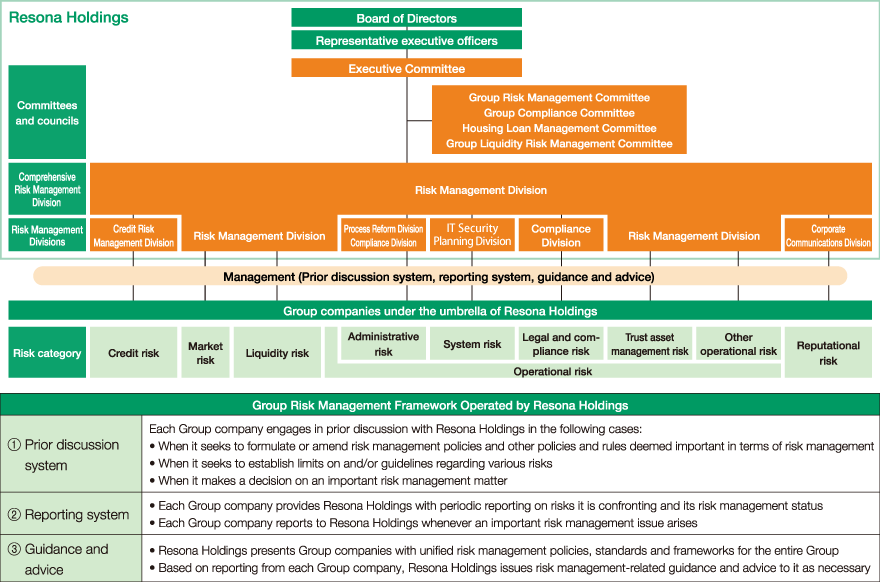

Group Management by Resona Holdings

Qualitative Risk Management

The Company provides Group banks and other Group companies(hereinafter collectively "Group companies") with direction and suggestions regarding risk management policies, standards, and systems that must be shared by all Group members. When making decisions on important matters related to risk management, Group companies confer with the Company in advance and base their decisions on those consultations or decide matters through the exchange of opinions, and report those decisions to the Company as necessary.

Based on the framework described above, the Company maintains a firm grip on risk management policies, standards and systems in place at each Group company, thereby ensuring qualitative risk management for the Group.

Quantitative Risk Management

The Company and the Group banks have in place comprehensive risk management systems as described later, with the aim of quantitatively assessing risks and controlling them within the tolerable limits.

Furthermore, the Company maintains the quantitative management of risks each Group company is handling through prior consultation on limits and guidelines or through the exchange of opinions.

Group companies must report to the Company regarding the risk conditions and their management on a regular and as-needed basis so that the holding company can provide guidance and advice as necessary.

Under the Management Committee and various other committees, we have formed risk management divisions by risk category within the Company to manage each type of risk on a Groupwide basis.

Group Risk Management System

Comprehensive Risk Management and Capital Allocation

Comprehensive risk management divisions have been formed within the Company and the Group banks, and these divisions are each responsible for the comprehensive risk management of their respective Group company or bank.

Each Group bank measures the volume of credit risk, market risk and operational risk using such risk management indicators as value at risk (VaR)* and establishes risk limits (makes risk capital allocations) on these types of risk. Risk management is conducted to control risk within these established limits.

When the Group banks set their risk limits, the Company verifies the details of the limits to be established to confirm the soundness of the Group as a whole. Also, the Company receives periodic reports from the Group banks regarding the status of risk management and confirms the status of comprehensive risk management of the Group.

In addition, although the Company is constantly working to improve the quality of risk measurement through various means, including the application of the VaR method, there are risks that cannot be quantified by statistical risk management methods. The Group strives to study and understand the incompleteness and specific weak points of the VaR method, thereby assessing and recognizing the impact of such limitations on risk measurement.

For risks that cannot be identified or quantified by the VaR methhod, the Company and the Group banks conduct qualitative assessment through various stress testing and the use of risk-assessment mapping. In this way, the Group aims to enhance the quality of its comprehensive risk management.

- *VaR, or value at risk, is a risk management indicator that is calculated using statistical methods to measure the maximum loss that may occur within a specified confidence interval (probability) and over a specified period.

Stress Tests

The Group carries out a variety of stress tests, each assuming a massive economic deceleration, turmoil in financial markets or other similar scenario aimed at confirming its resilience against and capital adequacy in a stressful environment and thereby verifying the appropriateness of its management plan and assessing the impact of differing risk factors on its operations.

Stress tests being carried out in the course of formulating a management plan employ multiple stress scenarios, including some deemed highly likely to materialize and some that would gravely impact the Group’s operations. In this way, the Group measures the possibility of an increase in losses associated with its risk-weighted assets and fluctuations in profit due to deterioration in revenues over a period spanning multiple fiscal years.

Stress tests are utilized to evaluate the stability of the Group’s revenues, assess how its capital adequacy would be impacted by the assumed stresses and prevent excessive risk-taking.