Our Response to Climate Change- and Nature-Related Issues (initiatives related to the TCFD and TNFD recommendations)

Resona Holdings will deepen its efforts in line with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) and the Task Force on Nature-related Financial Disclosures (TNFD) and will work to expand its disclosures.

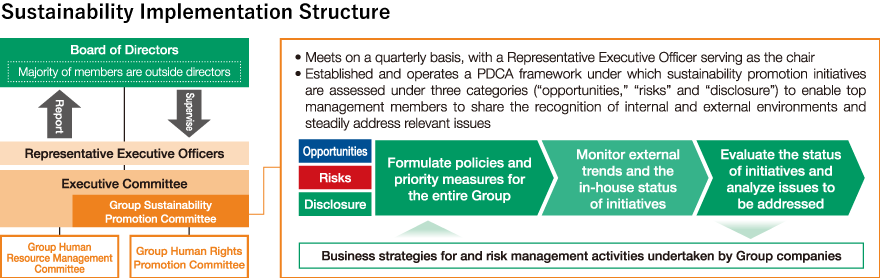

Governance

The Board of Directors is responsible for overseeing responses to climate change and nature-related issues as an important element of sustainability initiatives. Please refer to "Sustainability Implementation Structure" for specific oversight structures and status. The Board of Directors has also established the Resona Group Environmental Policy, which includes supporting international environmental norms and engaging in dialogue with stakeholders, including business partners, to improve efforts on climate change and biodiversity in line with those norms. In addition, bearing in mind that environmental issues are closely related to human rights and local communities, the Board of Directors has also established the Resona Group Policy on Human Rights, which includes supporting international human rights norms and engaging in dialogue with stakeholders, including local communities, to improve efforts on respect for human rights in line with those norms.

Policy and Implementation Structure

Management Strategy (Climate Change)

Business Opportunities and Risks Arising from Climate Change

To measure the impact of climate change, which is highly unpredictable, we have undertaken qualitative and quantitative evaluations of opportunities and risks based on two different scenarios involving, respectively, a 1.5℃ and a ℃ rise in global temperatures.

This evaluation includes the assessment of estimated impact in the short-, medium- and long-terms, which are defined as approximately 5-, 15- and 35-year periods, respectively.

1.5℃ scenario

reference: IEA Net-Zero Emissions by 2050, IPCC RCP2.6 and other publicly approved scenarios

Projected developments

- GHG emissions from businesses are severely restricted by government-led policies and laws

- Advances in and the popularization of low-carbon technologies enhances the availability of low-carbon alternatives to existing products and services

- Frequency of sudden occurrences of abnormal weather remains virtually unchanged

Impact on the financial industry

Financing streams will be ever more focused on measures to alleviate climate change impact

Time frame

Short to long term

Projected financial impact

Opportunities

| Product and service markets |

|

|---|---|

| Resource efficiency, energy sources, and market resilience |

|

Risks

Transition risks

| Policy and legal |

|

|---|---|

| Technology and market |

|

| Reputation |

|

Physical risks

| Acute |

|

|---|---|

| Chronic |

|

4℃ scenario

reference: IPCC RCP8.5 and other publicly approved scenarios

Projected developments

- Without notable breakthroughs in climate change countermeasures, the volume of overall GHG emissions continues to grow at the current pace

- Due to an increase in the number of sudden occurrences of abnormal weather, society suffers even more significant damage

- Chronic and irreversible changes, such as a sea level rise, affect economic activities undertaken by businesses and individuals

Impact on the financial industry

Financing streams will be ever more focused on measures to adapt to climate change effects

Time frame

Short to long term

Projected financial impact

Opportunities

| Product and service markets |

|

|---|---|

| Resource efficiency, energy sources, and market resilience |

|

Risks

| Transition risks |

|

|---|---|

| Physical risks (Acute・Chronic) |

|

In-Depth Qualitative Analysis of Climate Change Scenarios

We recognize that the risks and opportunities described above could result in a significant financial impact on our portfolio of loans, which represents the Group’s largest asset.

Based on this recognition, we have selected priority sectors requiring urgent action from among carbon-related sectors specified by the TCFD. Targeting these sectors, we conducted an in-depth analysis of climate change scenarios.

Currently, these priority sectors comprise (1) “Energy / Utility,” (2)“Transportation / Automotive” and (3) “Real estate development / Construction.”

Process Used to Select Priority Sectors

|

|

|---|---|

|

|

|

|

|

|

| Sector | Climate change impact | Portfolio size | Scale of GHG emissions volumes | Selection results |

|---|---|---|---|---|

| Energy / Utility | Large |

Small |

Large |

Priority sector(1) |

| Transportation / Automotive | Large |

Medium |

Large |

Priority sector(2) |

| Real estate development / Construction | Medium |

Large |

Medium |

Priority sector(3) |

| Material | Large |

Small |

Large |

Not selected*2 |

| Agriculture / Food | Medium |

Small |

Small |

Not selected |

| Pulp / Forestry products | Large |

Small |

Small |

Not selected |

- *1Large: More than 5 trillion yen; Medium: ¥1 trillion to ¥5 trillion; Small: Less than 1 trillion yen

- *2Not selected due to differing risk characteristics associated with each type of material and the resulting segmentation of the portfolio

Formulation of Scenarios for Each Priority Sector and the Qualitative Analysis of Developments in Climate Change-related Risks

Targeting each priority sector, we formulated scenarios and conducted a qualitative analysis regarding the magnitude of climate change impact and the timing of its materialization.

|

With reference to information publicized by the TCFD, the UNEP FI and the SASB, conduct surveys and identify important factors considered to exert a profound impact on risks and opportunities affecting each sector |

|---|---|

|

Analyze important factors identified via 1 above and assume the magnitude of climate change impact and the timing of its materialization based on highly objective parameters recommended by the International Energy Agency and other bodies that support a scientific approach. Incorporate findings from this analysis into the "Five Forces Analysis"*3 to hypothesize the future status of society and thereby assess the impact on priority sectors |

|

Formulate certain scenarios and assess developments in climate change-related risks in each sector |

- *3A method of sector analysis accounting for impacts attributable to sellers, buyers, newcomers and alternatives, with policies considered as an element affecting all other factors

1. Important factors associated with risks and opportunities in each sector

| Energy / Utility | Transportation / Automotive | Energy | |

|---|---|---|---|

| Policy | Introduction and/or heightening of carbon tax | Introduction and/or heightening of carbon tax | Introduction and/or heightening of carbon tax |

| Legal | Tightening of GHG emission regulations | Tightening of GHG emission regulations | Strengthening of environment-related building regulations |

| Market | Popularization of renewable energy | Rising energy prices | Shift in customer needs to buildings with higher environmental performance |

| Reputational | Higher customer awareness regarding the need to address environmental concerns | - | - |

| Technology | - | Transition to electric vehicles | - |

| Acute | Surging expenses for the reinforcement of disaster countermeasures and the emergence of physical damage | Operational impact of a catastrophic disaster | Increasingly frequent occurrences of flooding and other natural disaster damage |

| Chronic | - | Damage to railroads due to heat expansion and rising air conditioning expenses (transportation) | - |

2. The future status of society and possible impact on each sector

Energy / Utility

| Future status of society | Impact on sector | |

|---|---|---|

| 1.5℃ | Initiatives aimed at achieving carbon neutrality advance significantly, leading to the introduction of a carbon tax and the growing popularization of renewable energy | The use of renewable energy gains popularity at an ever-faster pace with the move toward carbon neutrality |

| 4℃ | Physical risks rise due to the continued dependence on fossil fuels | While fossil fuel demand grows solidly, the sector is affected by frequent occurrences of damage arising from abnormal weather and surging disaster countermeasure costs |

Transportation / Automotive

| Future status of society | Impact on sector | |

|---|---|---|

| 1.5℃ | Initiatives aimed at achieving carbon neutrality advance significantly, leading to the introduction of a carbon tax, the popularization of renewable energy and EVs and the acceleration of modal shift in the transportation sector | Toward carbon neutrality, the use of eco-friendly vehicles and rail cars gains growing popularity, resulting in the acceleration of modal shift |

| 4℃ | Physical risks rise as the transition to a low carbon society fails to gain further momentum | While the market environment remains unchanged, the sector is affected by frequent occurrences of damage arising from abnormal weather and surging disaster countermeasure costs |

Real estate development / Construction

| Future status of society | Impact on sector | |

|---|---|---|

| 1.5℃ | Initiatives aimed at achieving carbon neutrality advance significantly, leading to the enforcement of carbon taxation, the introduction of building materials with low carbon footprint and the growing popularization of renewable energy | The construction of facilities designed to reduce environmental burden progresses at an ever-faster pace |

| 4℃ | Rising physical risks lead to growing demand for buildings with greater disaster resilience | While the construction of facilities equipped with greater resilience against flooding and other disasters progresses, the sector is affected by frequent occurrences of damage arising from abnormal weather and surging disaster countermeasure costs |

3. Developments in climate change-related risks(L:Low risk, M:Medium risk, H:High risk)

Energy / Utility

| 2030 | 2035 | 2040 | 2045 | 2050 | |

|---|---|---|---|---|---|

| Transition risks: 1.5℃ Scenario | H |

H |

H |

H |

H |

| Physical risks: 4℃ Scenario | H |

H |

M |

M |

M |

Transportation / Automotive

| 2030 | 2035 | 2040 | 2045 | 2050 | |

|---|---|---|---|---|---|

| Transition risks: 1.5℃ Scenario | M |

H |

H |

H |

H |

| Physical risks: 4℃ Scenario | M |

M |

M |

M |

M |

Real estate development / Construction

| 2030 | 2035 | 2040 | 2045 | 2050 | |

|---|---|---|---|---|---|

| Transition risks: 1.5℃ Scenario | L |

L |

L |

L |

L |

| Physical risks: 4℃ Scenario | H |

H |

H |

H |

H |

| Priority sectors | Transition risks : 1.5℃ Scenario | Physical risks : 4℃ Scenario |

|---|---|---|

| Energy / Utility | Risk becomes constantly high around 2030 based on an assumption that the use of fossil fuel will decrease due to the enforcement of carbon taxation, across-the-board efforts to achieve carbon emission reduction targets and changes in the energy mix | Risk becomes constantly high from 2030 onward based on an assumption that monetary damage arising from flooding will increase approximately 20%, and then subsides to medium in line with an assumed increase in crude oil prices (approximately 30%) in 2040 and resulting growth in revenue |

| Transportation / Automotive | Risk remains medium based on an assumption that demand for vehicles with internal combustion engines (ICEs) will significantly decline in 2030 due to carbon taxation and the enforcement of stricter regulations on such vehicles. However, risk becomes constantly high from 2035 onward due to the enforcement of domestic regulations on the marketing of new ICE vehicles in the 2030s, provided that falling demand is not compensated for by demand for eco-friendly vehicles | Risk rises to and remains at medium from 2030 onward based on an assumption that monetary damage arising from flooding will increase approximately 20% |

| Real estate development / Construction | Risk remains low based on an assumption that an increase in costs attributable to a possible increase in the regulatory pressure to lower energy consumption intensity will be offset by growing revenue backed by rising demand for net-zero energy buildings (ZEBs) in 2040 | Risk becomes constantly high from 2030 onward based on an assumption that monetary damage arising from flooding will increase approximately 20% |

In-Depth Quantitative Analysis of Climate Change Scenarios

Based on the qualitative analysis, we conducted a quantitative analysis of the impact on the Group’s financial performance of transition and physical risks.

Transition risks (1.5℃ Scenario)

The characteristics and magnitude of transition risks’ financial impact vary by sector. Also, these factors may be altered going forward by measures undertaken by businesses pursuing carbon neutrality. Accordingly, our qualitative analysis has targeted priority sectors selected via qualitative analysis. In addition, we have positioned “introduction and/or heightening of carbon tax” as an important risk factor to be used as an assumption for our scenario in light of the universal impact of such taxation on each sector. Moreover, in reference to publicly approved scenarios, we have assumed a 1.5°C rise in global temperature to assess the resulting future impact on our clients. In this way, we estimated our exposure to credit risks that may emerge during the period leading up to 2050.

| Target Sectors | All the priority sectors (“Energy / Utility,” “Transportation / Automotive” and “Real estate development / Construction”) |

|---|---|

| Assumptions for the Scenario | The assumed impact on the Group’s credit risk exposure is based on additional expenses that would be incurred by clients due to the introduction and/or heightening of carbon tax as well as future business responses to the growing public call for carbon neutrality |

| Reference Scenarios | IEA Net-Zero Emissions by 2050 and IPCC 2.6 |

| Analysis Period | Present to 2050 |

| Risk Indicator | Estimated increase in credit-related expenses |

| Analysis Results | Credit-related expenses could increase during the period leading up to 2050 by a maximum of around 93.0 billion yen |

Physical risks (4℃ Scenario)

Physical risks are considered to have a differing degree of impact on clients depending on the locations of both their businesses and real estate properties pledged as collateral for loans in addition to sector-specific characteristics of their operations. Taking this into account, our quantitative analysis targeted business corporations in general. Due to restrictions in data available for analysis, we have positioned flood damage resulting from the materialization of acute risk as an important factor to be used as an assumption for our scenario. In reference to publicly approved scenarios, we have thus estimated the impact of a 4°C rise in global temperature on the business performance of our clients and real estate properties pledged as collateral for loans, determining its impact on the Group’s credit risk exposure during the period leading up to 2050.

| Target Sectors | Business Corporations in General |

|---|---|

| Assumptions for the Scenario | Based on analyses of hazard maps and natural disaster models, we have estimated the frequency of flooding arising from the materialization of acute risk and resulting growth in flood damage. Having assessed the impact of the above factors on the business performance of clients and their real estate properties pledged as collateral for loans, we have thus determined the extent to which the Group’s credit exposure would be affected |

| Reference Scenarios | IPCC RCP8.5 |

| Analysis Period | Present to 2050 |

| Risk Indicator | Estimated increase in credit-related expenses |

| Analysis Results | Credit-related expenses could increase during the period leading up to 2050 by a maximum cumulative total of around 14.0 billion yen |

Action to Be Taken Based on Results of Scenario Analysis

The results of the preceding scenario analysis suggest that the impact of transition and physical risks on credit costs can be considered limited. However, we believe that these results are not indicative of the full impact on the Group’s overall risk exposure, as the above analysis has taken into account only a portion of the relevant risk factors while using various assumptions in the course of damage estimation.

The analysis of climate change impact requires the study of a diverse range of risk factors and their intertwining relationships. Moreover, the spillover effect of climate change-related risks could evolve depending on various underlying factors. Therefore, we will continue striving to enhance the accuracy of our analysis.

At the same time, even though we are in the process of developing more precise analysis methods, we are convinced that climate change is highly likely to have a financial impact on our loan assets, the largest category of assets in the Group’s possession.

Accordingly, we clearly recognize that the opportunities and risks our clients face will directly affect the Group.

The majority of the Group’s loan assets are accounted for by loans furnished to individual and SME customers. This suggests that climate change-related lending risks are dispersed throughout our overall portfolio. However, it was confirmed that, compared with large corporations, the status of SMEs’ climate change responses varies widely by company, indicating a diverse range of underlying issues confronting this customer group.

Looking ahead, we will not only increase the sophistication of scenario analysis but also upgrade the methods used to assess and monitor the volume of financed emissions, even as we engage in in-depth customer dialogue and enhance our solutions. In this way, we will assist our customers in their pursuit of carbon neutrality.

Management Strategy (Nature-Related Issues)

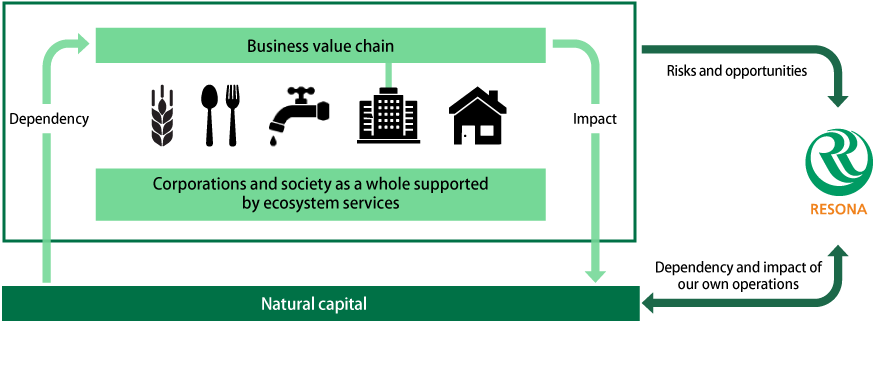

Relationship between Businesses, Including Financial Institutions, and Natural Capital

Financial institutions, like ourselves, not only affect natural capital through direct business operations but also maintain a broad and in-depth relationship with such capital through their lending to and investment in corporate and individual customers. Accordingly, these institutions have a responsibility to ensure that nature-related issues are handled properly.

Risks and opportunities arising from our clients’ dependency and impact on natural capital are directly linked with risks and opportunities the Resona Group itself faces. With this in mind, the Group promotes the careful analysis of its portfolio of loans, which represents its largest asset, via the use of the LEAP Approach Guidance*4 stipulated under the TNFD’s information disclosure framework.

- *4Guidance on the identification and assessment of nature-related issues: The LEAP approach (issued by the TNFD in October 2023)

Nature-Related Risks and Opportunities for Clients

Risks

| Consequences arising from businesses with high dependency | Consequences arising from businesses with high | |

|---|---|---|

| Physical risks (chronic) |

|

|

| Physical risks (acute) |

|

|

| Transition risks |

|

|

Opportunities

| Consequences arising from businesses with high dependency | Consequences arising from businesses with high | |

|---|---|---|

| Resource efficiency, products and services |

|

|

Heat Map Analysis

Using ENCORE,*5 a tool specialized in nature-related risk analysis, we have conducted a heat map analysis of each sector in order to assess its degree of dependency and impact and also determined the proportion of the Group’s financing portfolio accounted for by each sector.

For detailed analysis results, please refer to p. 51 of the Resona Group Integrated Report 2025.

Integrated Report Fiscal Year 2024 | Financial Information | Resona Holdings, Inc.- *5Exploring Natural Capital Opportunities, Risks and Exposure

Management of Risks and Impact

The Resona Group has positioned risks that are deemed to possess a high possibility of impacting heavily on the Resona Group as top risks in order to develop a consistent risk management structure, placing the foremost emphasis on managing these risks.

Top risks recognized as being relevant to sustainability include “Deterioration in competitiveness, etc., due to changes in social and industrial structures,” “Changes in the earnings structure and deterioration in profitability, etc., due to the revision of laws, regulations, government policies, etc.,” and “Operational suspension, etc., due to the occurrence of natural disasters.”

We have also identified such main risk scenarios as “Loss of growth opportunities, the emergence of stranded assets and other issues due to delays in the response to climate change and biodiversity issues, etc., that negatively impact corporate value,” “Deterioration of corporate value due to the absence of information disclosure practices that can be considered sufficient by external stakeholders,” and “Operational suspension or other serious consequences, including a threat to human life, due to a major natural disaster, such as an earthquake, massive wind or flooding, or a pandemic.”

Top risks are determined via discussion at the Executive Committee, the Board of Directors and other important bodies. Through top risk management, the Company is striving to enhance risk governance, prevent the emergence of significant risks, ensure swift response to risk materialization and curb the spread of risk repercussions.

We have also clarified types and definitions of risks to be managed and the organizational structure for risk management as well as the fundamental risk management framework, with the aim of establishing a structure enabling us to manage various risks by using methodologies aligned with their characteristics.

To address credit risk, which is considered to have a particularly strong impact on the Group’s operations, we are working to step up risk management via, for example, “Initiatives for Socially Responsible Investing and Lending” described below.

Metrics and Targets

In 2021, the Resona Group established Long-Term Sustainability Targets for its long-term initiatives aimed at mitigating climate change-related risks and increasing opportunities. In May 2023, we announced our commitment to reach net zero emissions by 2050 in terms of Scope3 Category 15 greenhouse gas emissions resulting from our investment and loan portfolio. We also announced an interim target to lower emissions in the electric power sector2022.

Carbon Neutrality Target (Scope1+2)

| Categories | Target | Results for FY2024*6 |

|---|---|---|

| The Group’s greenhouse gas emissions (Scope1+2) | 70% reduction by FY2025 compared to FY2013 Net zero by FY2030 | 22,192t-CO2 (76% reduction from the FY2013 level) |

| Of which, Scope1 | 40% reduction by FY2025 compared to FY2013 | 4,321t-CO2 (48.7% reduction from the FY2013 level) |

| Of which, Scope2 | 80% reduction by FY2025 compared to FY2013 | 17,871t-CO2 (78.9% reduction from the FY2013 level) |

- *6Provisional

Declaration of Net-zero Greenhouse Gas Emissions in the Investment and Financing Portfolio Interim target for 2030 for the energy sector

| Categories | Target | Results for FY2024 |

|---|---|---|

| Greenhouse gas emissions from investment and loan portfolio (Scope3 Category 15) | Net zero by FY2050 | - |

| Of which, electric power sector: carbon intensity | 100~130 gCO2e/kWh |

145 gCO2e/kWh |

Retail Transition Financing Target

| Categories | Target | Results for FY2024 |

|---|---|---|

| Financing aimed at helping retail customers update their awareness, transform their modes of behavior and stably move forward from their current situation *Includes non-environmental sectors |

Cumulative total of transition financing from FY2021 to FY2030: 10 trillion yen | Approx. 1.9 trillion yen (of which, financing in the environment-related fields: 570 billion yen) |

Please refer to the links below for details of each target, progress made so far, and future initiatives.

Carbon Neutrality Target (Scope1+2) Declaration of Net-zero Greenhouse Gas Emissions in the Investment and Financing Portfolio Retail Transition Financing Target